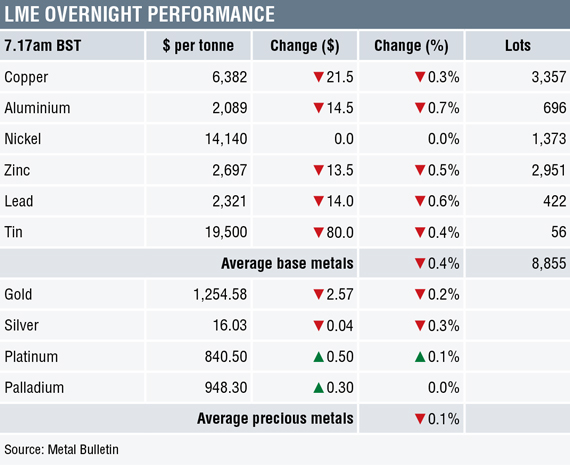

Three-month base metals prices on the London Metal Exchange broadly continued their recent run of weakness on the morning of Thursday July 5. Nickel prices were unchanged, while the rest of the complex was down by between 0.3% for copper ($6,382 per tonne) and 0.7% for aluminium ($2,089 per tonne).

Volume has been above average with 8,855 lots traded as at 7:17am London time.

This follows a generally weak performance on Wednesday, when the complex closed down by an average of 1.2%, with only aluminium ending the day in positive territory.

In precious metals this morning, gold and silver spot prices were down by 0.2% and 0.3% respectively, with gold at $1,254.58 per oz, while palladium was little changed and platinum was up by 0.1% at $840.50 per oz – the recent low being $797 per oz and the lowest since December 2008.

The precious metals managed to find some buying on Wednesday, with the complex closing up by an average of 0.4%.

In China, base metals prices on the Shanghai Futures Exchange were down across the board by an average of 2.4%, led by a 4.5% drop in the most-traded August zinc contract. The most-traded August copper contract was down by 2.6% at 49,460 yuan ($7,457) per tonne.

In other metals in China, the September iron ore contract on the Dalian Commodity Exchange was down by 1.3% at 456.50 yuan per tonne. Meanwhile on the SHFE, the October steel rebar contract was down by 0.4%, the December gold contract was unchanged and the December silver contract was down by 0.1%.

Spot copper prices in Changjiang were down by 1.9% at 49,530-49,880 yuan per tonne and the LME/Shanghai copper arbitrage ratio was at 7.75.

In wider markets, spot Brent crude oil prices were off by 0.48% at $77.77 per barrel this morning. The yield on US 10-year treasuries continued to weaken – it was recently quoted at 2.8461%, while the German 10-year bund yield was firmer at 0.3200%.

Asian equity markets were for the most part weaker on Thursday: Nikkei (-0.78%), Hang Seng (-0.97%), CSI 300 (-0.56%), the Kospi (-0.35%), while the ASX200 closed up by 0.52%. This follows a firmer performance in European markets on Wednesday, where the Euro Stoxx 50 closed up by 0.17% at 3,412.03.

The dollar index at 94.28 is weakening after establishing a double high at 95.54 (June 21 and 28). The euro is firmer and is getting some lift off low ground at 1.1704, as is sterling at 1.3246, while the yen and the Australian dollar are consolidating at 110.58 and 0.7383 respectively.

The continuing tensions over trade with the United States has weakened the yuan in the past few weeks, but in recent days it has started to consolidate lower off the lows – it was recently quoted at 6.6313 after a low of 6.7167 on July 3. Most of the emerging currencies we follow are also consolidating after recent weakness, the exception being the peso which continues to rebound.

Economic data already out this morning shows Germany’s factory orders rising 2.6% in May, after a 1.6% fall previously. Data out later includes EU retail purchasing managers’ index (PMI), UK housing equity withdrawals as well as US releases that include Challenger job cuts, ADP non-farm employment change, initial jobless claims, final services PMI, ISM non-manufacturing PMI, crude oil inventories and the minutes from the Federal Open Market Committee’s June meeting.

In addition, Bank of England governor Mark Carney and German Bundesbank president Jens Weidmann are speaking. One old piece of data worth noting is that US total vehicle sales climbed to 17.5 million units in June, up from 16.9 in May – this data was released on Tuesday.

The washout in base metals prices continues – it was particularly strong on Wednesday but that was probably a result of thinner trading with the US on holiday. With the LME nearby spreads tighter and most backwardated it does look as though the sell-off in prices is attracting short-covering and nearby buying interest. In this ‘falling knife’ environment we would wait for a buying opportunity, but the tightening spreads may well suggest the sell-off is close to running its course.

Our medium-term view is not bearish; we still feel this year’s weakness is the market adjusting to the strength seen in 2016 and 2017, but further tightness in supply lies ahead. Needless to say the US’ stance on trade is undermining confidence and until those tensions die down, buyers may feel in no need to restock.

The precious metals have been hit hard on the downside and the fact they have not featured as a haven bid during the US trade negotiations suggests they are out of favor with investors now that other havens are paying a higher yield. Platinum prices are looking particularly weak with prices $413 per oz lower than those of gold.

The post METALS MORNING VIEW 05/07: Sell-off continues, but tighter spreads suggest short-covering appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News