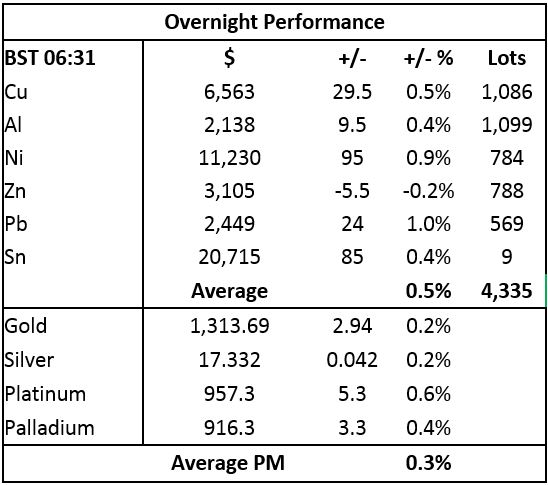

Base metals prices on the London Metal Exchange are up by an average of 0.5% this morning, Wednesday September 20. Most metals are in positive territory, with three-month copper prices up by 0.5% at $6,563 per tonne, although zinc prices, down by 0.2%, are bucking the uptrend. Volume has been below average with 4,335 lots traded as of 06:31 BST.

This follows a mixed day of trading on Tuesday that saw average gains of 0.4%, with increases in aluminium (+1.7%) and lead (+1.3%), copper and zinc prices were little changed, while tin and nickel were weaker by 0.5% and 0.3%, respectively.

Precious metals prices are firmer by an average of 0.3% this morning, led by platinum that is up by 0.6%, followed by palladium prices that are up by 0.4%, while gold and silver prices are up by 0.2%, with spot gold prices at $1,313.69 per oz. This follows a day of strength for bullion prices on Tuesday that saw gold prices close up by 0.2%, silver prices climb by 0.6%, while the platinum group metals (PGMs) suffered with palladium prices falling 2.4% and platinum prices closing down 0.7%.

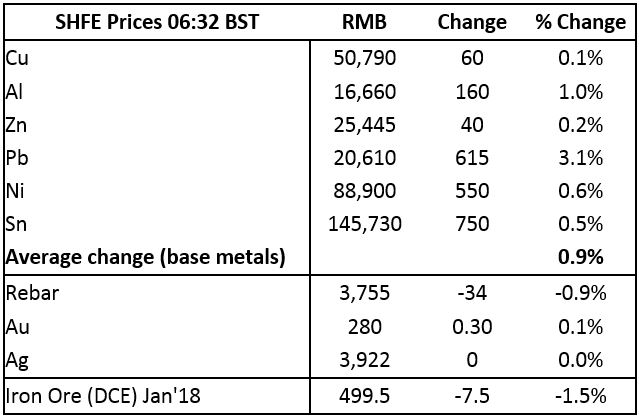

On the Shanghai Futures Exchange (SHFE) this morning, the base metals are up across the board by an average of 0.9% – this follows a 1.7% gain at this time on Tuesday. Lead prices once again are leading the way with a 3.1% climb, followed by a 1% gain in aluminium prices, with nickel and tin up by 0.6% and 0.5%, respectively, while zinc prices are up by 0.2% and copper lags with a 0.1% gain to 50,790 yuan ($7,712) per tonne. Spot copper prices in Changjiang are also up by 0.1% at 50,700-50,860 yuan per tonne and the London/Shanghai copper arb ratio has eased to 7.75, from 7.77 on Tuesday.

On Tuesday, the slide in the rebar and iron ore prices appeared to have halted, but prices are weaker again this morning, with steel rebar on the SHFE off 0.9%, while January iron ore prices are down 1.5% at 499.50 yuan per tonne on the Dalian Commodity Exchange. Gold and silver prices on the SHFE are little changed.

In international markets, spot Brent crude oil prices are down by 0.13% at $55.30 per barrel and the yield on US ten-year treasuries has firmed to 2.24%, while the German ten-year bund yield is little changed at 0.45%.

Asian equities are mixed this morning with the Nikkei and Kospi little changed, the Hang Seng is up by 0.3%, the CSI 300 is up by 0.5% and the ASX 200 is off by 0.1%. This follows another positive session on Tuesday in the USA where the Dow closed up by 0.18% at 22,370.80, while in Europe, the Euro Stoxx 50 climbed 0.13% to 3,531.18.

The dollar index at 91.70 appears to be drifting lower again after its attempt to rally last week. This suggests the market does not expect much shift in the US Federal Reserve’s stance when the Federal Open Market Committee (FOMC) statement is issued this evening. As the dollar drifts, the euro at 1.2014 is climbing as is the Australian dollar at 0.8030, sterling is consolidating in high ground at 1.3525 and the yen’s slide has halted at 111.40.

The Chinese yuan has been weakening since September 8 – it reached 6.5968 on Tuesday, but was recently quoted at 6.5637, so seems to be consolidating. Other emerging market currencies are looking mixed with the rupee weaker at 64.362, the rupiah is giving back some of its recent gains, the rand is weak at 13.3032, while the ringgit is firm at 4.1910.

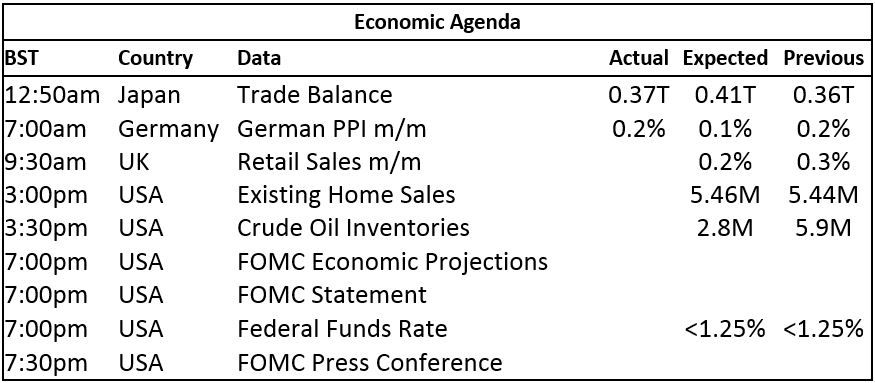

Data out already shows strong Japanese trade data with imports and exports beating expectations, which bodes well for the country’s economy as well as the state of the global economy. German PPI climbed by 0.2%, unchanged from the previous reading but better than expected. Later, UK monthly retail sales are due along with a host of US data including existing home sales and crude oil inventories, with the FOMC economic projections, statement, interest rate decision and press conference.

Aluminium prices suffered the least during last week’s correction and prices are now leading on the upside and extending gains. Lead prices are looking strong, followed by copper and zinc prices, while nickel appears to have run into enough buying to halt its price slide and tin prices are stuck sideways – but are well placed to break higher. As such, it does look like the recent sell-offs have run their course and buying is returning to varying degrees. The weaker dollar may well provide a tailwind, although whether the FOMC statement gives the dollar another boost remains to be seen.

The weaker dollar seems to be lending gold prices some support as did US president Donald Trump’s rhetoric at the UN on Tuesday. Given the stalemate over North Korea and the likelihood that tension will escalate again before too long, we would expect gold to remain in demand and for dips to be supported, as seems to be the case. If the FOMC statement does not point to any acceleration in monetary policy tightening then gold prices may well be able to work higher again. If gold prices do suffer a sell-off on the back of the statement then we would expect that to lead to an even better buying opportunity. For now, we see gold’s weakness as part of a test of its break out level ($1,295 per oz) and so far prices have held above that level. Silver continues to follow gold’s direction, while the PGMs are looking slightly heavier.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW: Gold’s sell-off halts; rhethoric over North Korea, weaker dollar provide support appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News