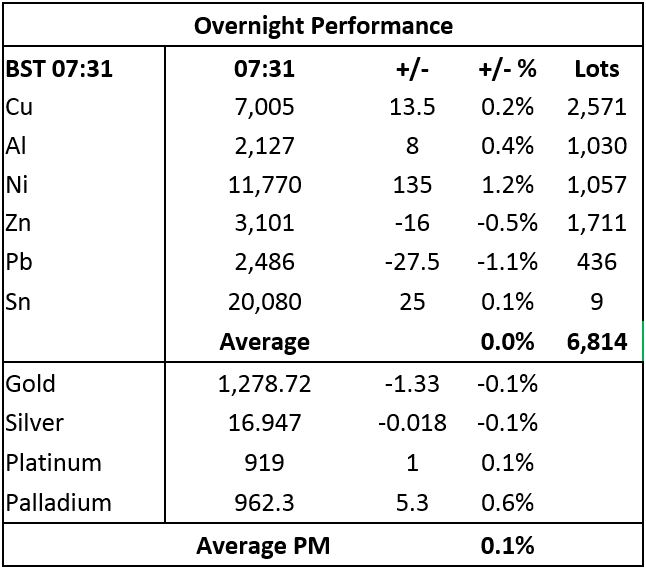

Base metals prices on the London Metal Exchange are broadly higher this morning, Thursday October 19. Nickel prices lead the gains with a 1.2% increase to $11,770 per tonne, while tin, aluminium and copper prices are up by between 0.1% and 0.4%, with three-month copper prices at $7,005. Lead and zinc are bucking the trend, with prices down by 1.1% and 0.5%, respectively.

Volume has been average at 6,814 lots as of 07:31 BST.

This morning’s trading follows a market of two-halves on Wednesday that saw copper, aluminium, tin and nickel prices decline by between 0.7% and 1.6%, while lead and zinc prices were up by 0.7% and 1.4%, respectively. So Wednesday’s gainers are the metals under pressure this morning and vice versa.

Gold, silver and platinum prices are little changed this morning, while palladium prices are up by 0.6% as they recoup some of Wednesday’s 2.2% losses. The other precious metals were also weaker yesterday, with bullion prices down by 0.4% and platinum prices were off by 1.5%.

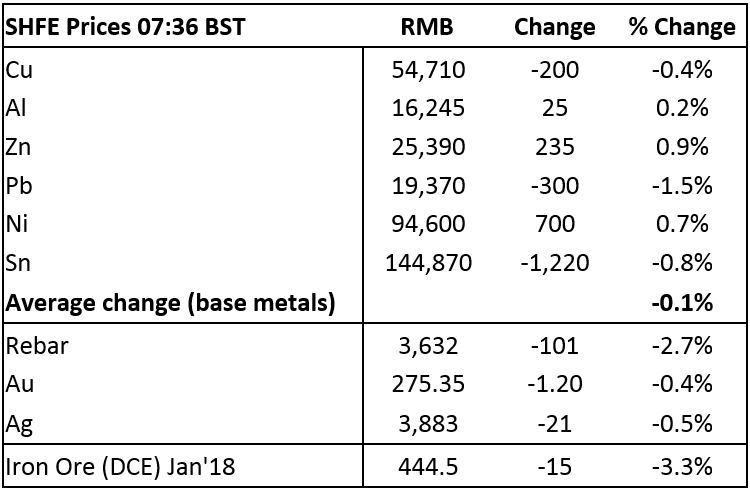

Base metals on the Shanghai Futures Exchange (SHFE) are split this morning. Lead is leading the decline with prices off by 1.5%, followed by tin and copper prices, down by 0.8% and 0.4% respectively, with the latter at 54,710 yuan ($8,260) per tonne. Meanwhile, zinc prices are up by 0.9%, nickel prices are firmer by 0.7% and aluminium prices are up by 0.2%.

Spot copper prices in Changjiang are down by 0.6% at 54,800-55,050 yuan per tonne while the London/Shanghai copper arbitrage ratio has eased to 7.81, compared with 7.82 on Wednesday.

The steel-orientated metals in China are again weaker with iron ore prices falling by 3.3% to 444.50 yuan per tonne on the Dalian Commodity Exchange, while steel rebar prices on the SHFE are down by 2.7% and gold and silver prices are off by 0.4% and 0.5%, respectively.

In international markets, spot Brent crude oil prices are off by 0.03% at $58.16 per barrel. The yield on US ten-year treasuries has firmed to 2.34% and the German ten-year bund yield is also firmer at 0.39%.

Equities in Asia are mixed: the CSI 300 and Hang Seng are both off by 0.5%, the Kospi is off 0.4%, the Nikkei is up 0.4% and the ASX 200 is up 0.1%. This follows an upbeat day on Wednesday, where in the USA, the Dow closed up by 0.7% at 23,157.60 – further extending the record high to 23,172.93 and in Europe where the Euro Stoxx 50 closed up by 0.33% at 3,619.65. Interesting that the bullishness in the Dow on Wednesday, combined with robust Chinese gross domestic product (GDP) data released this morning have not underpinned a broad-based firmer tone in Asia.

The dollar index has fallen back into consolidation mode at 93.30, it has started to oscillate sideways either side of 93.50 – the jury is still out as to whether this is a pause in the downward trend that has been in effect all year, or whether it is the start of a turning point for a move higher. The euro at 1.1813 is edging higher within a consolidation pattern, while sterling at 1.3196 is weaker, as are the yen at 113.02 and the Australian dollar at 0.7866.

The Chinese yuan has been weaker in the past few days, recently quoted at 6.6218, while the other emerging currencies we follow are generally on a back footing, although the Mexican peso is consolidating after its recent weakness.

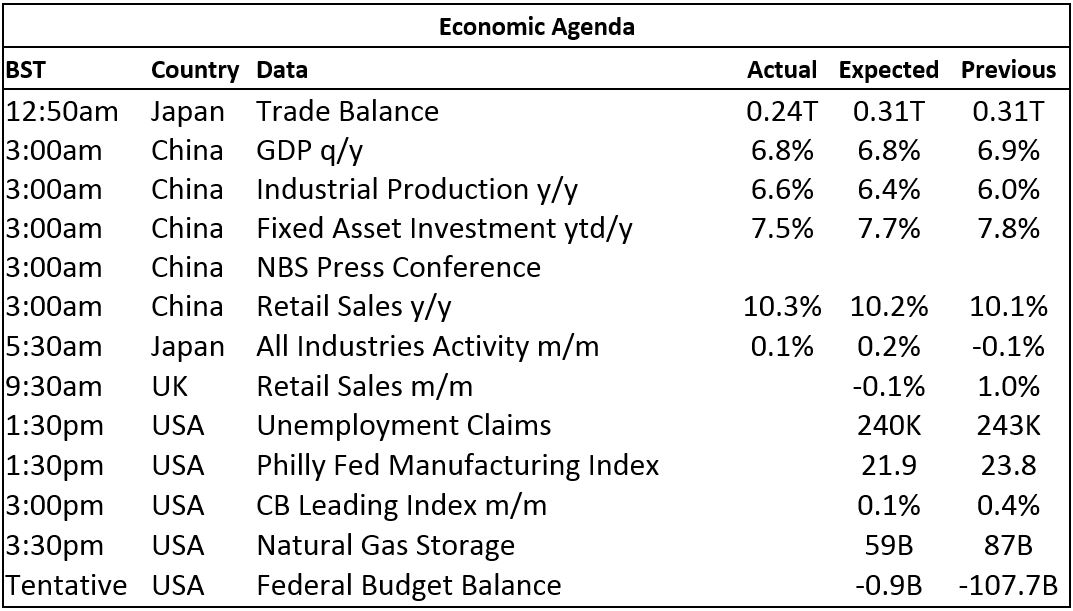

Data out earlier today included Japan’s trade balance and all industries activity; China’s GDP (6.8%); firmer industrial production at 6.6%, compared with 6% previously; weaker fixed asset investment growth of 7.5%, compared with 7.8% preciously and firmer retails sales at 10.3%, compared with 10.1%. Data out later includes UK retail sales, as well as US data including initial jobless claims, the Philly Fed manufacturing index, leading indicators, natural gas storage and the federal budget balance.

Scale-up selling has hit copper after Tuesday’s run-up to $7,177 per tonne but the pullback seems limited, suggesting there is dip buying into the pullback. The weakness in aluminium, zinc and lead also seems controlled with dip buying evident, while nickel prices have held up well and tin prices are suffering the most as prices failed to make headway above its recent break above $21,000 per tonne. We are on the lookout for signs about how strong underlying bullish sentiment is; recent turbulence with the price pullbacks, stock inflows and re-warranting of cancelled warrants, all surrounding the passing of the October date, have muddied the waters; so we wait to see how the market trades now the October date has passed. Our view of late has been to remain quietly bullish, but expect trading to become choppier when prices run into more bouts of scale-up selling – as indeed we seem to be experiencing.

The firmer tone in gold, silver and platinum prices has run out of steam and, with the dollar trying to push higher and equities hitting new highs, the opportunity cost of holding gold is high, especially while the North Korean situation seems to be calmer, at least for now. Palladium set a fresh high on Tuesday but prices are now consolidating – there is a risk of a double top on the chart but it is too early to say that will turn out to be the case while the overall uptrend still looks robust. We would expect the precious metals to remain well supported.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW: Gold prices finding some support above $1,275 per oz appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News