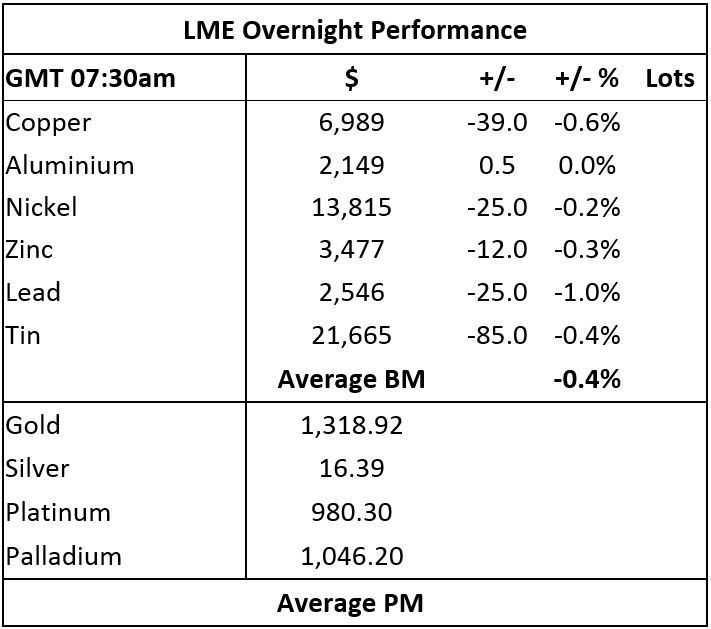

Precious metals prices dropped sharply yesterday on the back of hawkish talk from the new US Federal Reserve Chair Jerome Powell, with prices closing down an average of 1.3%, with spot gold prices closing at $1,318.15 per oz. This morning prices are consolidating with gold at $1,318.92 per oz, silver at $16.39 per oz, platinum at $980 per oz and palladium at $1,046.20 per oz.

We are not surprised by gold’s reaction to the latest Federal Reserve speak, we wait to see if the dollar breaks higher – if it does then we would expect that to be a headwind for gold prices, although given the possibility of equity and bond markets becoming more jittery, gold may attract more haven buying – so again we expect dips to be supported.

Base metals traded on the London Metal Exchange are mainly weaker this morning, Wednesday February 28, with prices off by an average of 0.4%.

Lead prices lead the decline with a 1% drop, followed by copper prices (-0.6%) at $6,989 per tonne. Tin, zinc and nickel prices are off between 0.2% and 0.4%, while aluminium prices are little changed.

This follows a day of general weakness on Tuesday that saw copper, nickel, zinc and lead prices drop an average of 0.8%, while aluminium and tin prices bucked the trend with gains of 0.4% and 0.8% respectively.

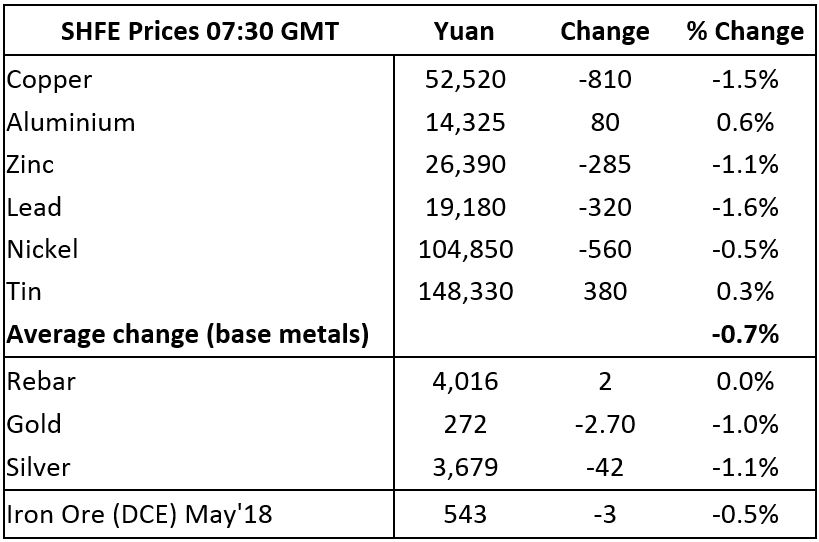

On the Shanghai Futures Exchange, the base metals are for the most part weaker, led by a 1.6% drop in lead prices and a 1.5% fall in copper prices to 52,520 yuan ($8,299) per tonne, with zinc prices down by 1.1% and nickel prices off by 0.5%. Aluminium and tin prices are bucking the trend with gains of 0.6% and 0.3% respectively. Spot copper prices in Changjiang are off by 1% at 52,300-52,480 yuan per tonne and the LME/Shanghai copper arbitrage ratio has edged out to 7.51, from 7.48 on Tuesday.

In other metals in China, iron ore prices are down by 0.5% at 543 yuan per tonne on the Dalian Commodity Exchange. On the SHFE, steel rebar prices are little changed, while gold and silver prices are off by around 1%.

In wider markets, spot Brent crude oil prices are weaker at $63.31 per barrel, while the yield on US 10-year treasuries is stronger at 2.9%, as is the German 10-year bund yield at 0.68%.

Equity markets in Asia are weak across the board this morning following Powell’s comments: Nikkei (-1.44%), Hang Seng (-1.54%), CSI 300 (-0.87%), ASX 200 (-0.68%) and Kospi (-1.17%). This follows weakness in western markets on Tuesday, where in the United States the Dow Jones closed down by 1.16% at 25,410.03, and in Europe where the Euro Stoxx 50 closed down by 0.15% at 3,458.03.

The dollar index’s rebound has restarted with the index recently quoted at 90.48 – yesterday’s high was 90.5, while the high from February 9 was 90.57. With a potential double bottom on the dollar index chart, a break up above 90.57 could well signal further dollar gains. The dollar strength is prompting weakness in the other currency majors: euro (1.2212), sterling (1.3887), yen (107.16) and Australian dollar (0.7801). The yuan has weakened too, moving to 6.3300 and the emerging market currencies we follow are all weaker too.

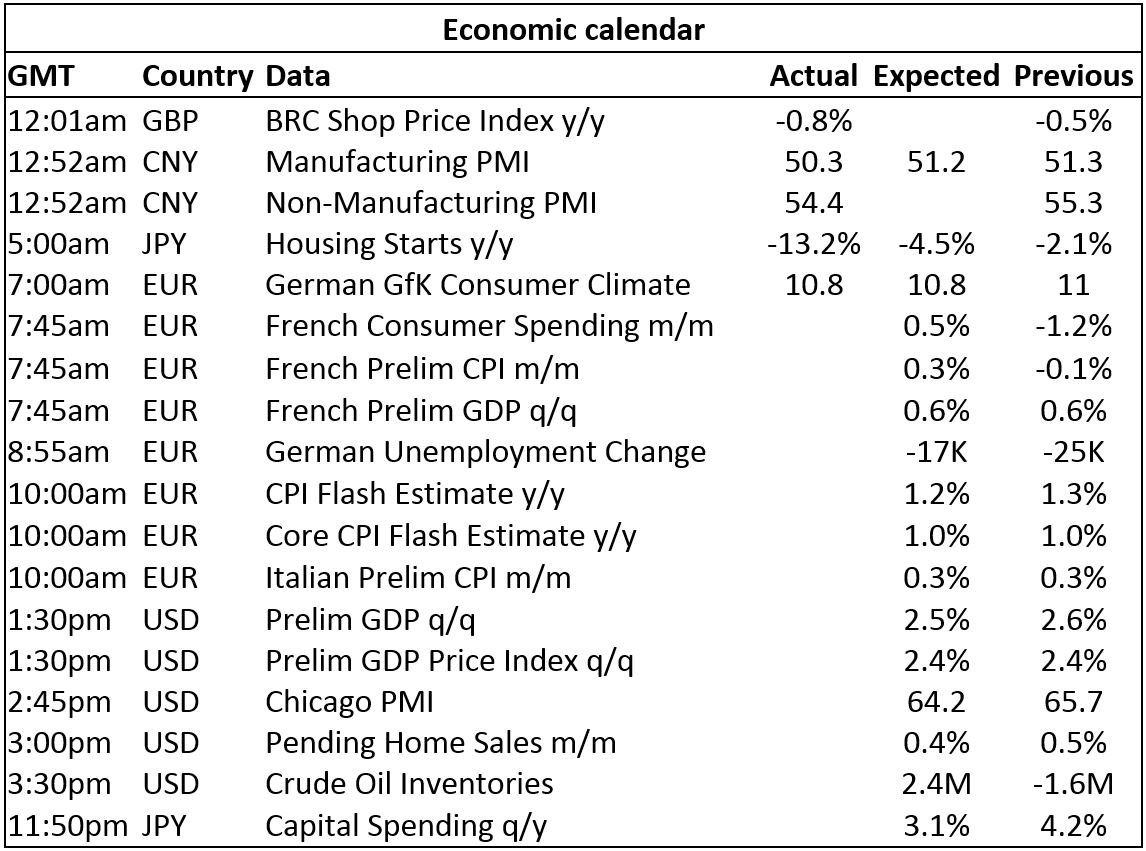

In addition to Powell’s hawkishness that took the market by surprise, Chinese purchasing managers’ index (PMI) data disappointed the market too with manufacturing PMI falling to 50.3, from 51.3, and non-manufacturing PMI dropping to 54.4, from 55.3. How much of the weakness is due to the Lunar New Year holiday remains to be seen. Japan’s housing starts fell and German GfK consumer climate eased to 10.8 from 11. Data out later includes French consumer spending, French consumer price index (CPI) and gross domestic product (GDP), German unemployment change, EU and Italian CPI, US GDP, Chicago PMI, US pending home sales and crude oil inventories.

The base metals had generally been holding up well but were not making headway, so it seems as though disappointed liquidation selling has emerged. Once again, we wait to see how well supported the dips are. We would not be surprised if the reaction to the more hawkish Powell talk is a flash in the pan – but if tomorrow’s manufacturing PMI are weaker than expected, which they are generally expected to be, then prices may end up needing to consolidate for longer. Our underlying view remains bullish, given concerted global growth and supply restraints following the past five years of reduced producer capital expenditure, but for now prices seem in no rush to break higher, so may have further to test on the downside.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post Metals morning view: Gold prices dropped sharply after Fed’s hawkish comments appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News