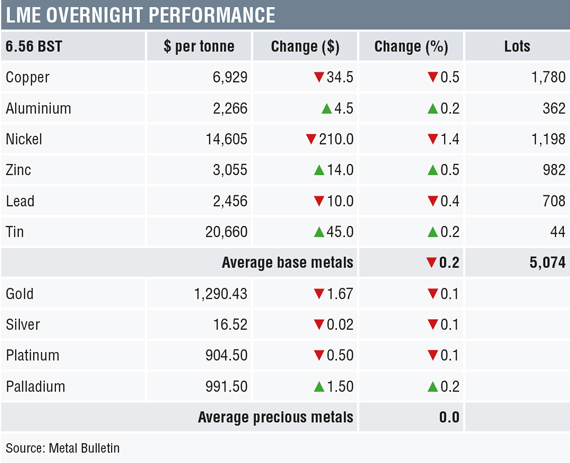

Three-month base metals prices on the London Metal Exchange were mixed on the morning of Wednesday May 23, with nickel and lead prices down by 0.4% and 1.4% respectively, while copper was off by 0.5% at $6,929 per tonne; aluminium and tin are both up by 0.2% and zinc is up by 0.5%.

Volume on the LME has been average with 5,074 lots traded as of 6.56am London time.

This follows a diverse performance on Tuesday when aluminium, zinc and tin closed down by an average of 0.7% and the rest of the complex closed up by an average of 0.6% – the two large movers being zinc that closed down by 1.9% and lead that closed up by 2.1%, which suggests a long zinc / short lead straddle trade is being unwound. The zinc-lead spread has narrowed to $581 per tonne from a peak of $1,035 per tonne in February.

Precious metals prices are little changed with gold, silver and platinum prices all off by 0.1% with spot gold at $1,290.43 per oz, while palladium prices are up by 0.2%. This follows a generally quiet session on Tuesday, although platinum prices did rebound 0.8% to $905 per oz.

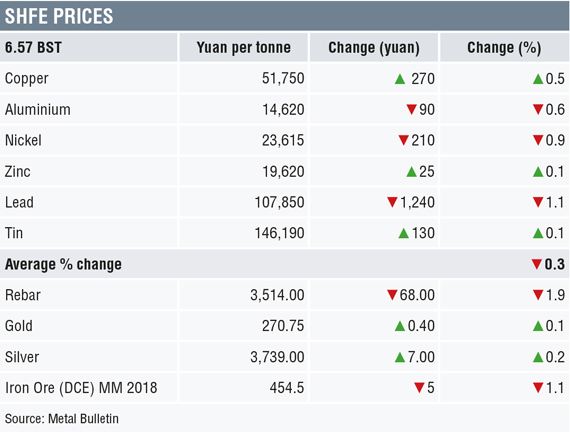

In China, copper prices on the Shanghai Futures Exchange were up by 0.5% at 51,750 yuan ($8,115) per tonne, lead and tin prices are both up by 0.1%, while aluminium, zinc and nickel are off 0.6%, 0.9% and 1.1% respectively.

Spot copper prices in Changjiang were up by 0.7% at 51,530-51,680 yuan per tonne and the LME/Shanghai copper arbitrage ratio has firmed to 7.47, from 7.46 on Tuesday.

In other metals in China, the ferrous metals continue to head lower with iron ore prices down by 1.1% at 454.50 yuan per tonne on the Dalian Commodity Exchange. On the SHFE, steel rebar prices were down by 1.9%, while gold and silver prices were up by 0.1% and 0.2% respectively.

In wider markets, spot Brent crude oil prices were down by 0.35% at $79.13 per barrel this morning. The yield on US 10-year treasuries has eased slightly to 3.0491% and the German 10-year bund yield has firmed to 0.54%.

Equity markets in Asia were for the most part weaker on Wednesday: Nikkei (-1.18%), Hang Seng (-1.01%), CSI 300 (-0.98%), the ASX 200 (-0.16%), but the Kospi climbed 0.46%. This follows a mixed performance in western markets on Tuesday, where in the United States the Dow Jones closed down by 0.72% at 24,834.10, and in Europe where the Euro Stoxx 50 closed up by 0.41% at 3,587.25.

The dollar index, at 93.73, is edging higher again, albeit still below Monday’s peak of 94.06. On the charts, there is likely to be resistance between 94.22 and 95.15.

The euro and sterling still look heavy at 1.1756 and 1.3399 respectively, the Australian dollar at 0.7543 is giving back more of Monday’s gains, although the yen is firmer at 110.38.

The yuan at 6.3786 is consolidating near recent lows. The Asian emerging market currencies we follow remain weak, while the peso, Real and rand have got some lift off recent lows.

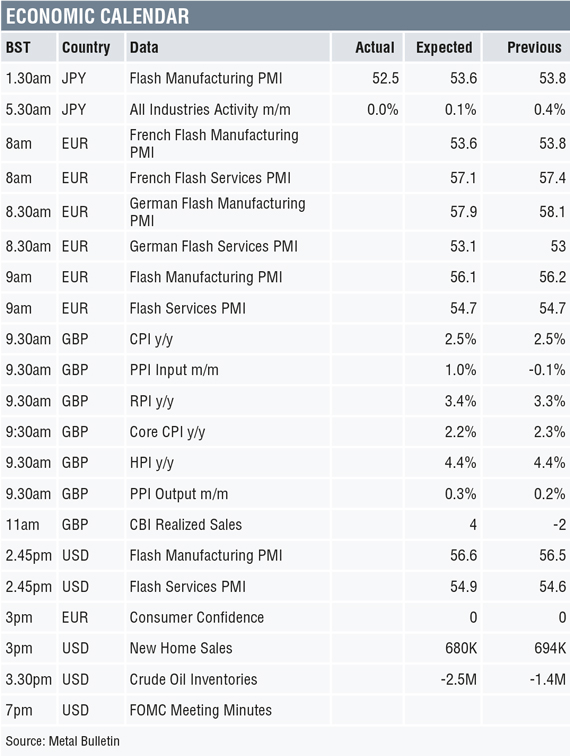

Today’s economic agenda is busy with flash PMI data out across most regions. In Japan, manufacturing PMI fell to 52.5 from 53.8 and all industries activity was flat after a 0.4% rise. In addition to the PMI data, there is data on UK PPI, CPI, HPI, RPI and realized sales. Other data includes EU consumer confidence, US new home sales and crude oil inventories, In addition, there is the release of the Federal Open Market Committee meeting minutes.

The base metals continue range-trading, with lead and nickel the ones with some upward direction, while the rest are heading flat-to-lower, suggesting generally balanced supply and demand. Without stronger economic growth the sideways trading is likely to continue, so today’s flash PMI data is likely to be watched closely for any signs of an economic pick-up or slowdown.

Gold prices have found support above $1,280 per oz and are consolidating either side of $1,290 per oz, platinum prices have also run into dip-buying, while silver and palladium prices have held up relatively better. The gold/silver ratio has pulled back to 78 from April’s highs above 82.

The post METALS MORNING VIEW 23/05: Metals stuck sideways; manufacturing PMI data in focus appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News