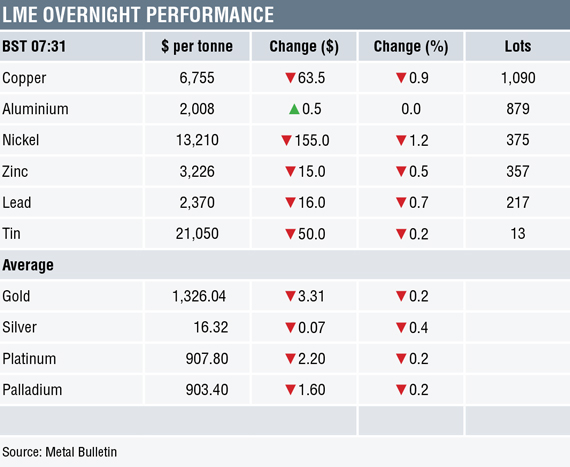

Base metals prices on the London Metal Exchange are for the most part weaker this morning, Friday April 6, following further announcements from the White House of increased tariffs against China.

The main movers are nickel (-1.2%), copper (-0.9%) at $6,755 per tonne, lead (-0.7%) and zinc (-0.5%), while tin and aluminium are little changed.

Volume remains light with 2,931 lots traded as of 07.31 am London time, this as China remains on holiday to mark the Qing Ming Festival, or tomb-sweeping day.

This morning’s performance follows a day of recovery on Thursday that saw the base metals complex close with gains averaging 0.9%.

Precious metals are down across the board this morning, which seems odd considering the overnight sell-off in metals and equities. Gold, platinum and palladium prices are all down by 0.2%, with gold at $1,326.04 per oz, while silver prices are down by 0.4% at $16.32 per oz. This follows a generally bearish day on Thursday that saw gold prices drop by 0.4%, platinum fall by 0.5% and palladium weaken by 2.5%, while silver bucked the trend with a 0.4% rise.

In wider markets, spot Brent crude oil prices are down by 0.85% at $67.89 per barrel and the yield on US 10-year treasuries is firmer at 2.82%, while the German 10-year bund yield remains at 0.51%.

Equity markets in Asia are for the most part weaker: Kospi (-0.33%), Nikkei (-0.36%), the ASX 200 (flat), while the Hang Seng is up by 1.09% – but having been closed on Thursday, it had some catching up to do. Thursday saw a strong rebound in western markets, where in the United States the Dow Jones climbed 0.99% to 24,505.22, and in Europe where the Euro Stoxx 50 closed up by 2.68% at 3,429.95.

The dollar index at 90.53 has moved up through the first (90.45) of the resistance levels we have been watching, the next is at 90.94 – a move above this would suggest an upside break. As the dollar strengthens, most of the majors are weaker: euro (1.2227), sterling (1.3987), yen (107.40), although the Australian dollar at 0.7668 is firmer. The yuan is giving flat at 6.3007, we wait to see how it reacts when the China’s back from holiday. The emerging market currencies we follow are on a back footing.

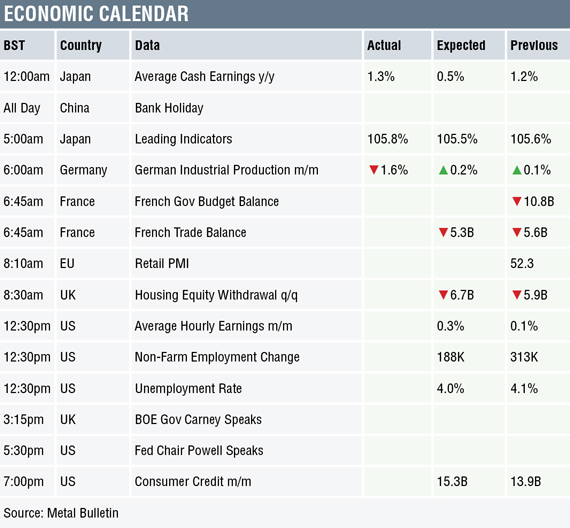

The economic calendar is focused on the employment report from the United States; non-farm employment is expected to rise by 188,000 and the unemployment rate is expected to drop to 4%. Data already out showed Japan’s average cash earnings rise 1.3%, up from 1.2% previously, and Japan’s leading indicators climb to 105.8% from 105.6%. Meanwhile, German industrial production dropped 1.6% – it was expected to rise 0.2%. Data out later includes France’s government budget and trade balance, the European Union’s retail purchasing managers’ index (PMI) and the United Kingdom’s housing equity withdrawals. As well as the US employment report there is also data on US consumer credit. In addition, the US Federal Reserve’s chair Jerome Powell and Bank of England governor Mark Carney are speaking.

The base metals are reacting to the trade rhetoric, having started to find some support in recent days, prices are weaker again this morning, but overnight trading will have been more pronounced as volumes have been light with China on holiday.

We wait to see if follow-through selling emerges, or whether traders shrug off the latest comments as more rhetoric. While the trade tensions last, i.e. until an agreement is reached – if one is, we would expect prices to consolidate further. Any let-up in trade tensions may well spark another round of buying from consumers and investors alike, especially as we are now in the second quarter, which is seasonally a stronger period for demand.

The fact gold prices have not reacted positively to the latest escalation in trade tariffs, while industrial metals and equities have sold off, suggests another round of risk-off. We wait to see if there is a secondary reaction – one of haven buying, which we may well see ahead of the weekend if trade tensions are not calmed by then.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW 06/04: More Trump rhetoric, more nervousness in metals markets appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News