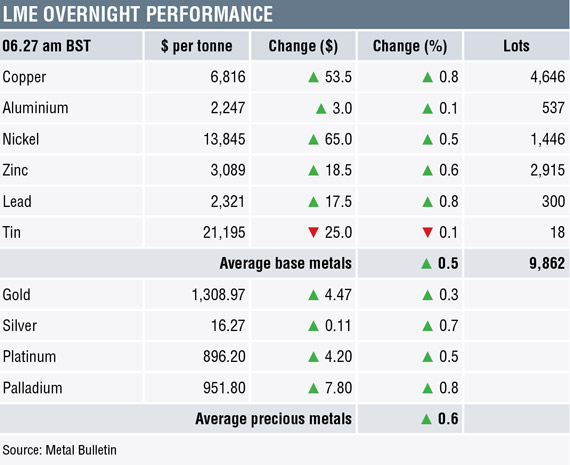

Base metals prices on the London Metal Exchange were for the most part firmer on the morning of Wednesday May 2, with five of the six base metals showing gains averaging 0.6%, while tin bucked the trend with a 0.1% decline. Copper led on the upside with a 1% gain to $6,816 per tonne.

Volume on the LME has rebounded with the return of Chinese participants following public holidays in China on Monday and Tuesday. There were 9,862 lots traded as at 06.27 am London time, this after an average volume of 1,710 lots at a similar time on Monday and Tuesday.

This follows a general day of weakness on Tuesday, when the complex closed down by an average of 0.4%, led by a 1.6% drop in zinc prices. Nickel (+0.8%) was the only metal to show gains on Tuesday.

The precious metals were all in positive territory this morning with gains averaging 0.6%, with gold prices up by 0.3% at $1,308.97 per oz. This after a weak performance on Tuesday when the complex was down by an average of 1.3%. We do wonder how much of the weakness in gold has been the market positioning itself ahead of this afternoon’s US Federal Open Market Committee (FOMC) rate decision and statement.

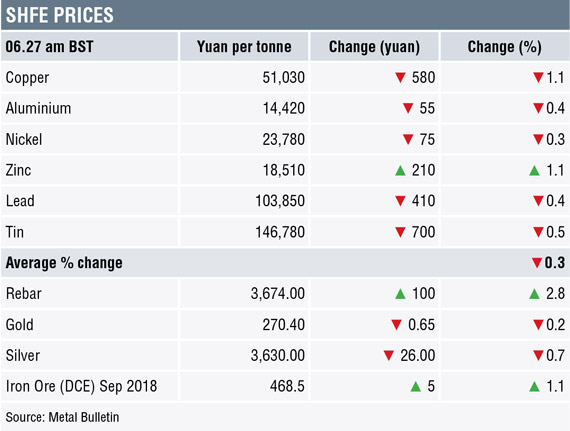

On the Shanghai Futures Exchange this morning, metals prices were for the most part weaker as they play catch-up having been closed for two days. Lead prices were the only ones in positive territory, with prices up by 1.1%, the rest were weaker with copper prices down by 1.1% at 51,030 yuan ($8,048) per tonne, while the rest saw losses of between 0.3% and 0.5%.

Spot copper prices in Changjiang were down by 1.7% at 50,710-50,850 yuan per tonne – the fact that futures were not off as much as the spot shows buying has come into the market since the spot price was set. The LME/Shanghai copper arbitrage ratio has firmed to 7.49 from 7.44 before the holidays.

In other metals in China, iron ore prices were up by 1.1% at 468.50 yuan per tonne on the Dalian Commodity Exchange. On the SHFE, steel rebar prices were up by 2.8%, while gold and silver prices were off by 0.2% and 0.7% respectively. We take some comfort from the fact basic raw material prices have opened up positively after the May 1 holiday.

In wider markets, spot Brent crude oil prices were weaker, with prices down by 0.21% at $73.18 per barrel, the yield on US 10-year treasuries was slightly firmer at 2.98%, and the German 10-year bund yield was little changed at 0.56%.

The equity markets in Asia are for the most part weaker: Nikkei (-0.22%), Hang Seng (-0.67%), CSI 300 (-0.04%), Kospi (-0.46%), while the ASX 200 is bucking the trend with a 0.59% gain. This follows a weaker performance in western markets on Tuesday, where in the United States the Dow Jones closed down by 0.27% at 24,099.05, and in Europe where the Euro Stoxx 50 closed little changed, off by 0.01% at 3,536.26 – not forgetting that most European equity markets were closed on Tuesday.

The dollar index at 92.44 continues to climb with the index clearly having broken out of a base formation that it has been in for most of the year – up until it broke higher on April 23. Dollar strength has weighed on other currencies: euro (1.1966), yen (109.79), sterling (1.3595) and the Australian dollar (0.7502). The yuan was weaker too at 6.3609, which is testing former support at 6.3625 from February 22. The emerging market currencies we follow were also on a back footing, suggesting some unrest over the stronger dollar and firmer US bond yields, which could increase the cost of servicing debt.

The economic agenda is busy today with data already out showing China’s Caixin manufacturing PMI edge higher to 51.1 from 51 – it was expected to come in at 50.9. Japan’s consumer confidence dipped to 43.6 from 44.3.

Later there is manufacturing PMI data out across Europe, as well as data on Italian and EU unemployment, UK construction, EU and Italian gross domestic product (GDP), with US data including ADP non-farm employment change, crude oil inventories and then this evening’s FOMC rate decision and statement. In addition, Germany’s Bundesbank President Jens Weidmann is speaking.

The base metals have been looking weak and the path of least resistance has been to the downside and that might have been accelerated on Tuesday given the thin trading conditions with China and most of Europe on holiday. Overall, we see the current weakness as being part of the drawn-out adjustment to the bullishness seen in 2016 and 2017, and with economic data now pointing to weaker growth, the markets have lost upward momentum. In turn, lack of upward momentum is leading to stale long liquidation. As such, we do not expect too much until we see better economic data and with that in mind we eagerly wait Europe’s PMI data this morning and the US employment report on Friday.

Precious metals prices are attempting to rebound this morning after a weak performance on Tuesday and overnight that saw gold, silver and platinum prices breach recent support levels. The strong dollar and firmer US treasury yields are a negative for precious metals, as is the general lackluster market condition. There has also been a trend of seeing weakness ahead of FOMC meetings, so we wait to see if gold prices pick up if the FOMC statement does not sound hawkish.

The post METALS MORNING VIEW 02/05: Metals prices rebound on recovery in volume after China returns appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News