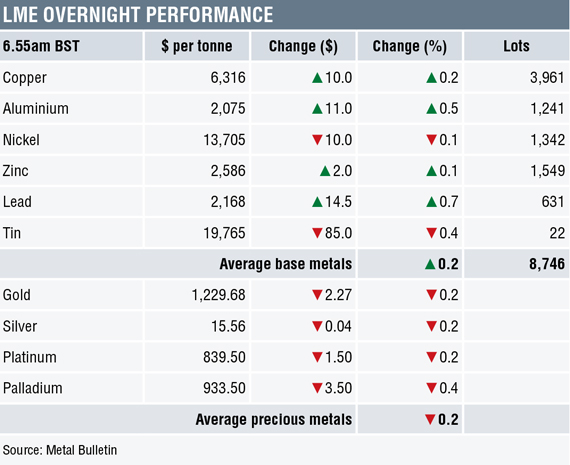

Three-month base metals prices on the London Metal Exchange were mixed on the morning of Thursday July 26, with lead leading on the upside with a 0.7% gain to $2,168 per tonne, while tin was the worst performer with a decline of 0.4% to $19,765 per tonne.

Copper was up by 0.2% at $6,316 per tonne – the high earlier this morning being $6,378 per tonne.

Volume has, however, been above average – some 8,746 lots had traded across the complex as at 6.55am London time.

Some progress on United States/European Union trade talks has provided some cheer in the market, but it is not all plain sailing with the trade rift between China and the US still wide open.

Precious metals were in consolidation mode on Thursday – spot gold, silver and platinum prices were all off by 0.2%, with gold at $1,229.58 per oz, while palladium prices were down by 0.4%.

This follows a firmer day on Wednesday that saw prices gain by an average of 1.3% – led by increases in the platinum group metals (PGMs).

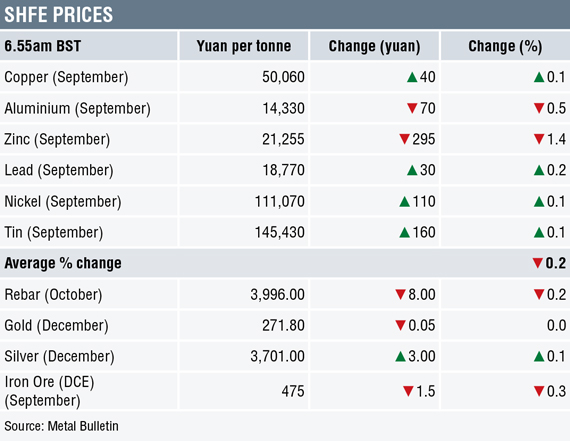

In China, base metals prices on the Shanghai Futures Exchange were similarly mixed; zinc was the main mover, with the metal’s most-actively traded September contract down by 1.4%, while the September aluminium contract fell by 0.5%. The rest were up between 0.1% and 0.2%, with the most-actively traded September copper contract up by 0.1% at 50,060 yuan ($7,386) per tonne.

Spot copper prices in Changjiang were up by 0.2% at 49,860-49,980 yuan per tonne and the LME/Shanghai copper arbitrage ratio has eased to 7.92, from 7.94 on Wednesday.

In other metals in China, the September iron ore contract on the Dalian Commodity Exchange was down by 0.3% at 475 yuan per tonne. On the SHFE, the October steel rebar contract was down by 0.2%, the December gold was little changed and the December silver was up by 0.1%.

In wider markets, spot Brent crude oil prices were down by 0.16% at $74.27 per barrel this morning. The yield on US 10-year treasuries was firmer at 2.9653%, while the German 10-year bund yield was also stronger at 0.4170%.

Asian equity markets were for the most part weaker on Thursday: Nikkei (-0.17%), Hang Seng (-0.64%), CSI 300 (-0.91%), ASX200 (-0.04%), while the Kospi climbed 0.64%. This follows a mixed performance in western markets on Wednesday; in the US, the Dow Jones closed up by 0.68% at 25,414.10, while in Europe the Euro Stoxx 50 closed down by 0.43% at 3,468.45, as the market prepared for the US/EU trade talks.

The dollar index at 94.14 is drifting again within its recent 93.71-95.66 range. On the chart, it looks like the dollar is building the right shoulder of a large inverse head-and-shoulder formation. Sterling (1.3199) and the yen (110.65) continue their rebounds, while the euro (1.1734) and the Australian dollar (0.7437) are firmer, albeit within recent ranges.

The yuan set a low at 6.8245 on Tuesday – it started to rebound on Wednesday, but was weakening again on Thursday and was recently quoted at 6.7804. The other emerging market currencies we follow were firmer, which may well indicate a return to risk-on.

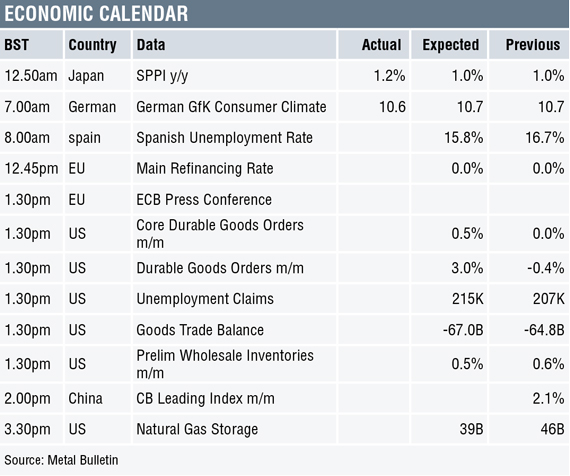

On the economic agenda, data out already shows a 1.2% gain in Japan’s services producer price index (PPI), while Germany’s GfK consumer climate reading eased to 10.6 from 10.7. Data out later includes the Spanish unemployment rate, the European Central Bank’s interest rate decision and press conference, along with US data includes initial jobless claims, durable goods orders, goods trade balance, wholesale inventories and natural gas storage. There is also data on China’s leading indicators later this afternoon.

Most of the base metals have found some support off their recent lows, but it is too early to say with confidence that the bases are in place as there are some fairly large overhead tails on recent candlesticks that suggest scale-up selling pressure.

Copper has been one of the bigger movers of late, but traders are likely to now wait for a decision from the labor union vote at the Escondida copper mine on July 28. In a number of the other metals, sideways trading within previous days’ ranges – which is most noticeable in zinc – suggests energy is building up for a directional move.

Given the extent of the sell-off since the June highs, we feel the metals have been looking oversold and the better flash purchasing managers’ index (PMI) data, combined with China’s move to support its economy in this tricky trade war environment, as well as some progress on US/EU trade talks, bodes well. Some of the key points over the next week will be the Escondida vote and China’s PMI data out on July 31.

The sell-off in gold prices has abated for now and prices are consolidating; silver is following gold’s lead, while the PGMs’ rebounds look stronger. For now we are neither bullish, nor bearish on gold and expect the precious metals to follow the lead of the metals complex as a whole.

The post METALS MORNING VIEW 26/07: Metals consolidate recent gains; markets likely to get nervous ahead of key events appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News