China’s manufacturing purchasing managers’ index (PMI) for May surprised to the upside at 51.9, having been expected to remain at April’s level of 51.4, though the positivity surrounding this release has yet to filter through to base metals prices on the London Metal Exchange.

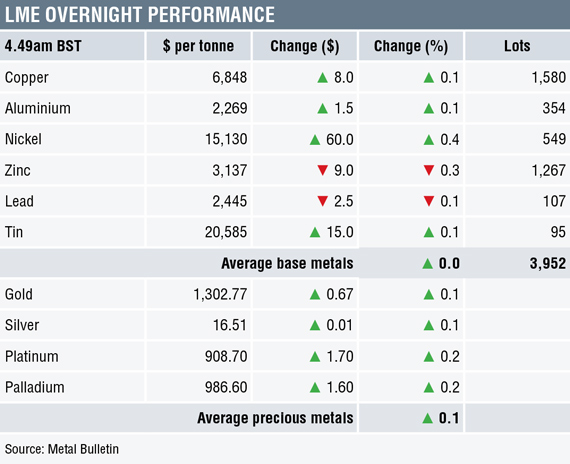

Three-month base metals prices on the LME were for the most part little changed during morning trading on Thursday May 31. Copper, aluminium and tin were up by 0.1%, with the red metal at $6,848 per tonne, zinc prices were up by 0.4%, while lead and nickel were down by 0.1% and 0.3% respectively.

Volume has been average with 3,952 lots traded as at 04:49 am London time.

This follows a generally firmer day on Wednesday when the complex closed up by an average of 0.8%, which was led by a 2.2% rebound in zinc prices, while aluminium prices struggled with a 0.1% loss.

The precious metals this morning were firmer with gold and silver prices up by 0.1%, with spot gold at $1,302.77 per oz, and platinum and palladium prices up by 0.2%. On Wednesday, gold and platinum prices were up by 0.1% and 0.2% respectively, while silver and palladium prices were more bullish with gains of 0.9% and 1% respectively.

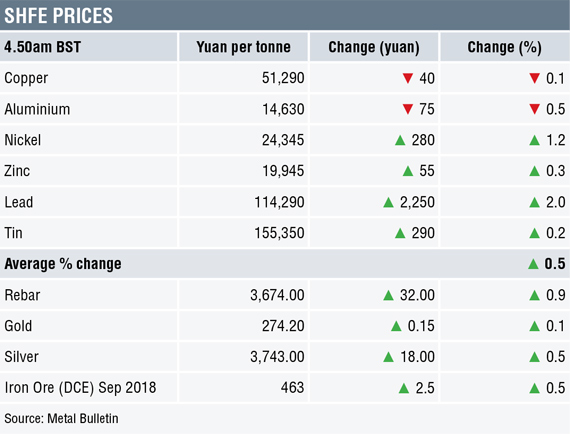

In China, base metals prices on the Shanghai Futures Exchange were diverging, with aluminium prices down by 0.5%, copper prices off by 0.1% at 51,290 yuan ($7,985) per tonne, while the rest were positive: nickel (+2.0%), zinc (+1.2%), lead (+0.3%) and tin (+0.2%).

Spot copper prices in Changjiang were unchanged at 51,050-51,170 yuan per tonne and the LME/Shanghai copper arbitrage ratio was weaker at 7.50, after 7.55 on Wednesday.

In other metals in China, iron ore prices were up 0.5% at 463 yuan per tonne on the Dalian Commodity Exchange. On the SHFE, steel rebar prices were up by 0.9%, while gold and silver prices were up by 0.1% and 0.5% respectively.

In wider markets, spot Brent crude oil prices were down by 0.5% at $77.44 per barrel this morning, this after a strong rebound on Wednesday. The yield on US 10-year treasuries was firmer at 2.8477%, as was the German 10-year bund yield at 0.3492%.

Equity markets in Asia were in recovery mode on Thursday: Nikkei (+0.72%), Hang Seng (+0.75%), CSI 300 (+1.56%), the ASX 200 (+0.47%) and Kospi (+0.57%). This follows a stronger performance in western markets on Wednesday, where in the United States the Dow Jones closed up by 1.26% at 24,667.78, and in Europe where the Euro Stoxx 50 closed up by 0.38% at 3,441.19.

The dollar index was little changed at 94.07, this after retreating on Wednesday to 94.09 from Tuesday’s high of 95.03. Resistance has held at 95.15 – the peak from October last year. Given the pullback in treasury yields this week, it is not too surprising the dollar has given back some ground, it also suggests some reduction in haven concerns over Italy’s political impasse where efforts are underway to form another government.

Most of the other major currencies that have been weaker on the back of the dollar’s strength are rebounding this morning: euro (1.1663), sterling (1.3302), the Australian dollar (0.7559), while the yen (108.77) that has been strong alongside the dollar is consolidating.

The yuan (6.4065) has also started to rebound, as have the rupiah, rand and ringgit, while the peso, rupee and Real are consolidating.

Today’s economic agenda is busy. Data out already showed Japan’s industrial production was up by 0.3% in April, after a 1.4% rise previously, and China’s non-manufacturing PMI edged higher to 54.9 from 54.8.

Data out later includes Japan’s housing starts, UK house price index, French consume price index (CPI), Italian monthly unemployment report, UK lending data, EU and Italian CPI and the EU unemployment rate. US data includes Challenger job cuts, initial jobless claims, personal income, spending and consumption expenditure, Chicago PMI, pending home sales and natural gas and crude oil inventories.

In addition, there is a G7 meeting and US Federal Open Market Committee members Raphael Bostic and Lael Brainard are speaking.

Copper prices bounced on Wednesday ahead of testing support at $6,710 per tonne – the low was $6,727 – and prices are now back in the sideways trading range that runs either side of the 20-day moving average at $6,860 per tonne.

Likewise, lead prices are now consolidating having dipped recently, zinc prices are continuing to rebound along with tin. Nickel continues its steady climb, while aluminium prices are little changed as they move sideways.

The pick-up in Chinese manufacturing PMI bodes well, but with a considerable amount of data out on Thursday and more PMI data and the US employment report out on Friday, the markets may delay making their mind up until they see all the data.

Gold prices are consolidating above $1,300 per oz and the weaker dollar seems to be helping in that regard. Silver, platinum and palladium are also consolidating. The complex seems to be waiting for fresh direction; for gold, this will probably come from the dollar and US treasury yields.

The post METALS MORNING VIEW 31/05: Rebound in Chinese manufacturing PMI bodes well for metals prices appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News