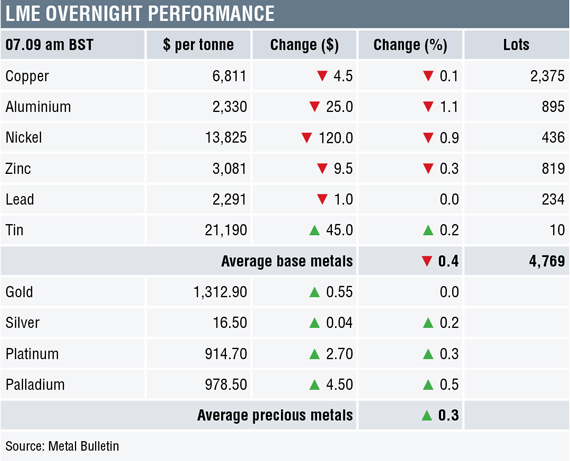

Base metals prices on the London Metal Exchange were more negative than positive on the morning of Thursday May 10, with all of the metals, except for tin (+0.2%) and lead (0.0%), down by an average 0.6%.

Aluminium prices led the decline with a 1.1% drop to $2,330 per tonne, while copper prices were down by 0.1% at $6,811 per tonne.

Volume on the LME has been below average, with 4,769 lots traded as at 07.09 am London time.

This follows on from a day of consolidating-to-firmer prices on Wednesday, when copper, aluminium and lead were little changed, while nickel, zinc and tin prices closed up between 0.3% and 0.5%.

The precious metals were firmer across the board with the complex up by an average of 0.3% – gold is the laggard with prices up just $0.55 per oz at $1,312.90 per oz.

This follows a mixed performance on Wednesday, where gold prices dropped by 0.2%, silver and platinum prices were little changed and palladium prices closed up by 0.5%. Considering the United States announced it was walking away from the Iran nuclear deal, we are surprised gold did not react more positively.

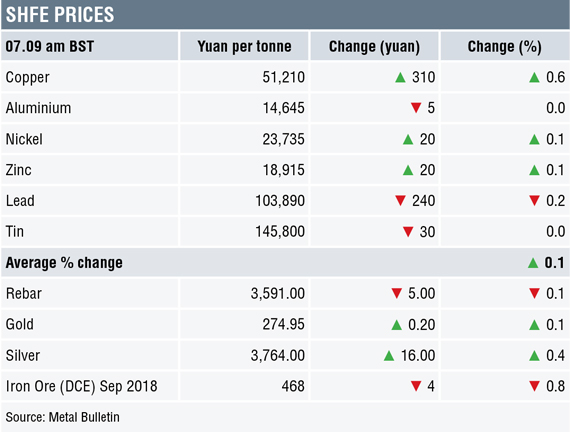

Copper prices on the Shanghai Futures Exchange this morning were up by 0.6% at 51,210 yuan ($8,039) per tonne, nickel prices were off by 0.2%, while the rest of the metals were little changed.

Spot copper prices in Changjiang were up by 0.3% at 50,840-51,000 yuan per tonne and the LME/Shanghai copper arbitrage ratio has edged up to 7.52 from 7.51 on Wednesday.

In other metals in China, iron ore prices were down by 0.8% at 468 yuan per tonne on the Dalian Commodity Exchange. On the SHFE, steel rebar prices were down by 0.1%, while gold and silver prices were up by 0.1% and 0.4% respectively.

In wider markets, spot Brent crude oil prices were up by 0.49% at $77.72 per barrel, underpinned by the US/Iran developments. Meanwhile, the yield on US 10-year treasuries eased back from the 3% level and was recently quoted at 2.98%, and the German 10-year bund yield eased to 0.55%.

Equity markets in Asia were largely up on Thursday: Nikkei (+0.39%), Hang Seng (+0.64%), CSI 300 (-0.01%), Kospi (+0.61%) and the ASX 200 (+0.17%). This follows a stronger performance in western markets on Wednesday, where in the US the Dow Jones closed up by 0.75% at 24,542.54, and in Europe where the Euro Stoxx 50 closed up by 0.33% at 3,569.74.

The dollar index is consolidating recent gains again, at 92.97, it is just hovering below Wednesday’s high of 93.42 – the uptrend looks strong, but it has already travelled 4.7% in an all but straight line since April 17 – so some consolidation may be needed. With the dollar rally pausing, most of the other major currencies have halted their slides: euro (1.1874), sterling (1.3567), and the Australian dollar (0.7469) are steady, but the yen remains on a back footing at 109.84. The yuan is also consolidating at 6.3639, but most of the emerging market (EM) currencies we follow remain on a back footing, although the rand and peso have managed to firm.

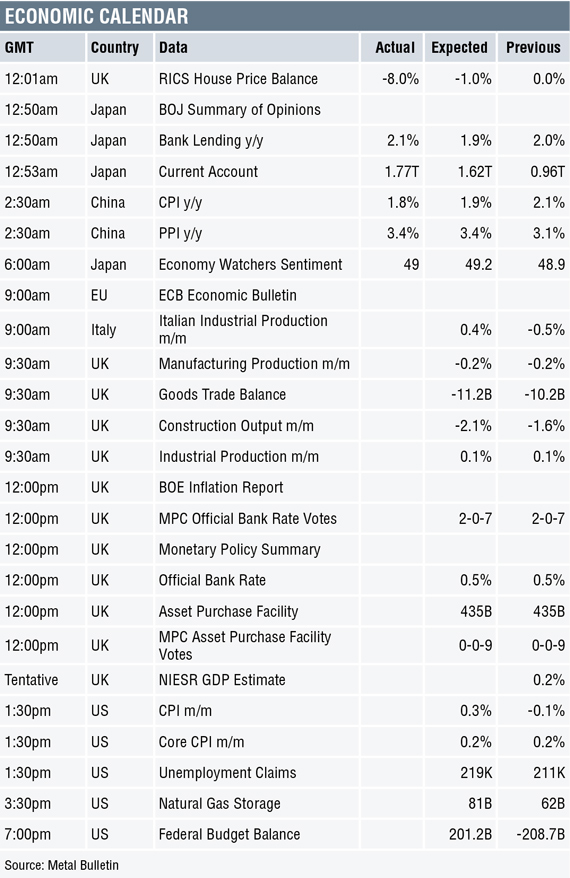

The economic agenda is very busy today – see table below. Of the data out so far, China’s consumer price index (CPI) has slipped to 1.8% from 2.1%, but its producer price index (PPI) has climbed to 3.4% from 3.1%.

There is a host of European data out later which includes a European Central Bank (ECB) economic bulletin, Italian industrial production and a raft of UK data including industrial and manufacturing production, goods trade balance, construction output, the Bank of England’s inflation report and monetary policy data and interest rate decision. There is also CPI, initial jobless claims, natural gas storage and the federal budget balance from the US of note.

The recent rebounds in aluminium, zinc and lead are consolidating, while copper, nickel and tin prices remain rangebound. The combination of less than bullish economic data, the strong dollar, rising yields, high oil prices and heightened geopolitical tensions all make for a risk-off environment. As such, we would not be surprised if prices came under more downward pressure. If that is avoided, however, then it will be a sign that demand is not weak, but it will reconfirm our belief that in the current climate consumers feel little need to chase prices higher.

The fact gold prices have failed to react bullishly to the increased geopolitical risk over Iran/US suggests there is a lack of interest in switching to risk-on trade. The opportunity cost of holding gold is also higher now that US treasury yields are firmer and the stronger dollar is a headwind too. If higher yields, a stronger dollar and geopolitical tensions start to undermine investor confidence in broader markets, then gold may start to pick up safe-haven buying.

The post METALS MORNING VIEW 10/05: Metals prices largely weak, markets awaiting fresh direction appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News