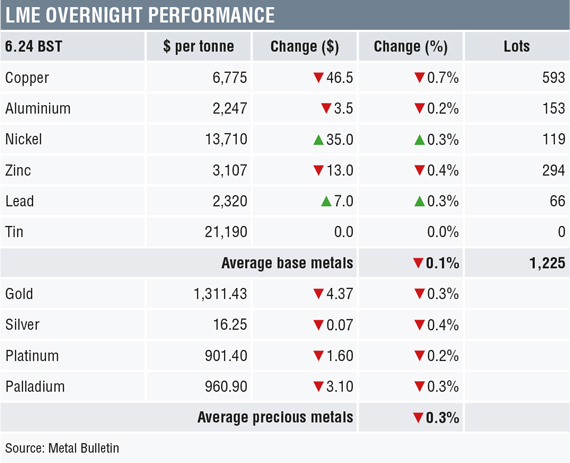

Base metals prices on the London Metal Exchange were mixed in the morning of Tuesday May 1, with copper (-0.7% at $6,775 per tonne), aluminium (-0.2%) and zinc (-0.4%) prices lower, while tin prices are untraded and lead and nickel prices are both up 0.3%.

Chinese markets are closed for a national holiday today, meaning volume has been light with 1,225 lots traded as of 6.24am London time.

This follows a diverse performance on Monday, that saw aluminium and tin prices rise 1.1% and 0.9% respectively, copper prices little changed, while nickel, lead and zinc prices fell 1.4%, 1.4% and 0.6% respectively.

Precious metals prices are down across the board this morning by an average of 0.3%, which has gold at $1,311.43 per oz. This follows weak performance on Monday when prices fell between 0.5-1% across the complex. The lackluster performance in the industrial metals, combined with a firm dollar, are weighing on the precious metals prices.

In wider markets, spot Brent crude oil prices were firmer, with prices up by 0.22% at $74.78 per barrel, the yield on US 10-year treasuries was little changed at 2.96%, and the German 10-year bund yield was easier at 0.56%.

The equity markets in Asia that are open are firmer with the Nikkei up 0.15% and the ASX 200 up by 0.58%. This follows a mixed performance in western markets on Monday, where in the United States the Dow Jones closed down by 0.61% at 24,163.15, and in Europe where the Euro Stoxx 50 closed up by 0.50% at 3,536.52. Most of Europe will be closed today for May Day holidays.

The dollar index remained firm at 91.90, the recent high being 91.99, and it looks as though the dollar is now heading higher having spent most of the year, up until recently, in a sideways base formation. This is likely to prove another headwind for metals prices. Conversely, the other major currencies we follow are on a back footing: euro (1.2067), sterling (1.3752), yen (109.39) and the Australian dollar (0.7539).

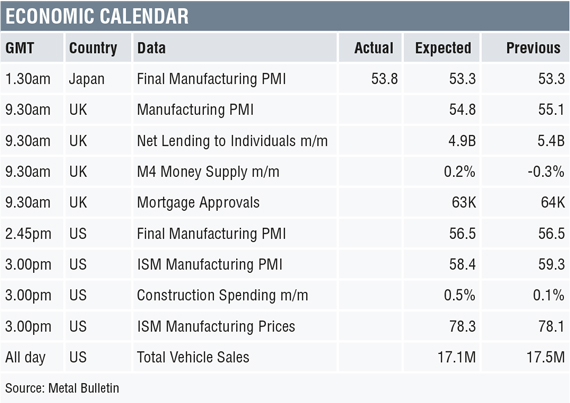

The economic agenda is busy today: data already out shows a rebound in Japan’s manufacturing PMI to 53.8 from 53.3; later there is PMI data out in the United Kingdom and the US. Other data being released today includes data on UK money supply and lending, with US data including construction spending, ISM manufacturing prices and total vehicle sales.

The base metals are on a back footing, with copper, zinc and nickel showing weakness, while the rest are just managing to tread water, although they also look vulnerable. We see the weakness as being part of the drawn-out adjustment to the bullishness seen in 2016 and 2017, and with economic data now pointing to weaker growth the markets have lost upward momentum. In turn, lack of upward momentum is leading to stale long liquidation. As such, we do not expect too much until we see better economic data – Japan’s PMI was a step in the right direction and we wait to see what today’s and tomorrow’s PMI data shows. On copper, last Friday’s CFTC data showed short-covering and a low gross short position, while the long position picked up for the second week running, this after a long drawn-out stretch of long liquidation. We wait to see if these are early signs that the funds are getting more interested again.

Precious metals prices are under pressure and support levels in gold around $1,302-1,307 per oz may now be retested. Platinum prices have broken recent support levels, while silver is holding up and palladium prices are retreating, but are still mid-range. It may be that gold prices are doing their usual pre-Federal Open Market Committee (FOMC) meeting sell-off ahead of Wednesday’s FOMC decision and statement.

The post METALS MORNING VIEW 01/05: Metals prices drift in absence of bullish news appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News