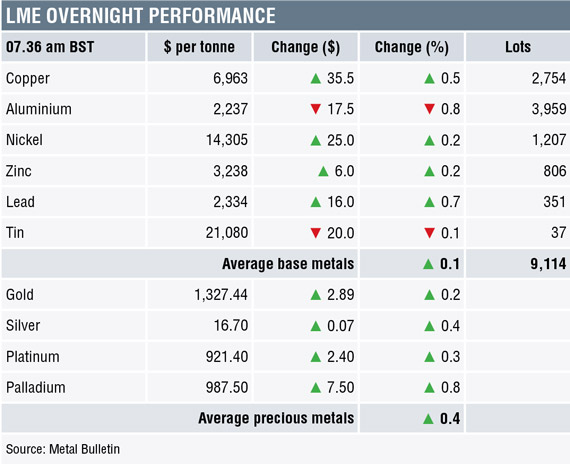

Base metals prices on the London Metal Exchange are for the most part firmer this morning, Tuesday April 24. The exceptions are aluminium (-0.8%) and tin (-0.1%), while the rest are up by an average of 0.4%, with three-month copper prices up by 0.5% at $6,963 per tonne.

On Monday, the United States Treasury’s decision that it will not impose secondary sanctions on non-US market participants for doing business with Russian supplier Rusal, helped to deflate the recent sanctions bubble.

Volume has been above average with 9,114 lots traded as of 07.46 am London time.

Precious metals prices are firmer this morning, with gains averaging 0.4% – led by a 0.8% rise in palladium prices to $987.50 per oz. This after a sharp correction on Monday following the latest developments on US sanctions against Russia. Gold prices also appear to have found support after their recent correction.

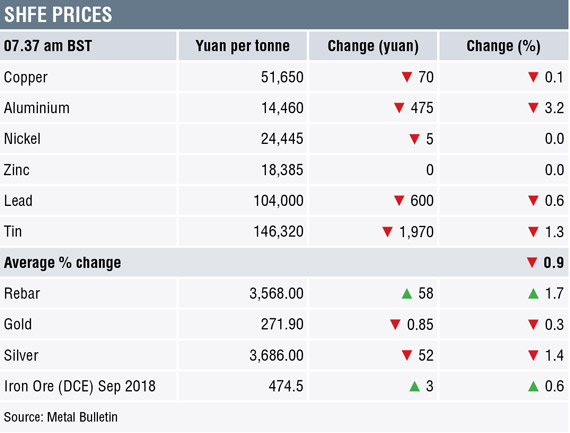

On the Shanghai Futures Exchange this morning, metals prices are split between being little changed and weaker with aluminium and nickel prices catching up with yesterday’s developments, with prices falling by 3.2% and 0.6% respectively, although tin prices are also down by 1.3%. Lead, zinc and copper prices are little changed, with the latter off by 0.1% at 51,650 yuan ($8,186) per tonne.

Spot copper prices in Changjiang are down by 0.4% at 51,560-51,800 yuan per tonne and the LME/Shanghai copper arbitrage ratio is at 7.42.

In wider markets, spot Brent crude oil prices are firmer, up by 0.1% at $75.07 per barrel and the yield on US 10-year treasuries is at 2.96%, with the German 10-year bund yield at 0.62%.

Equity markets in Asia are for the most part considerably stronger after geopolitical tensions seem to have eased between the US and Russia: Nikkei (+0.86%), the ASX 200 (+0.6%), Hang Seng (0.82%), and CSI 300 (1.83%), although the Kospi is bucking the trend with a 0.4% decline. This follows a mixed performance in western markets, where in the US the Dow Jones closed off 0.06% at 24,448.69, and in Europe where the Euro Stoxx 50 closed up 0.54% at 3,513.06. What is interesting is that the equities are not putting a negative spin on the stronger treasury yields.

Recent increases in geopolitical tensions and rising commodity prices, especially oil, seem to have spurred inflationary concerns that have led to stronger bond yields and in turn that has lifted the US dollar, with the dollar index at 90.97. This has broken above the previous peak at 90.94 from March 01.

This rise in the dollar seems to be weighing on gold and is likely to be a headwind for metals’ prices generally. With the dollar stronger, other major currencies are weaker: euro (1.2205), yen (108.85), sterling (1.3932) and the Australian dollar (0.7604). The yuan is also weaker at 6.3155 and the emerging market currencies we follow are all weakening, which may well be a warning sign rising concern about higher US treasury yields. So equities may be benefitting from the short-term relief of weaker currencies, but the weaker currencies may be an alarm bell we should be listening too.

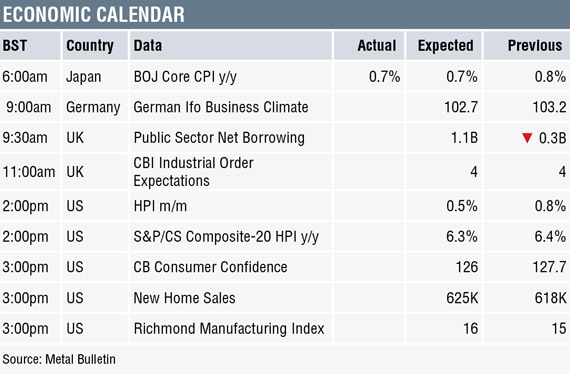

Data out already shows Japan’s core consumer price index (CPI) came in at 0.7%, slightly down from 0.8% previously. Later there is data on German Ifo business climate, UK public sector borrowing and CBI industrial order expectations, with US releases that include data on house prices, consumer confidence, new home sales and the Richmond manufacturing index.

In recent weeks the focus has been on aluminium, nickel, tin, palladium and the oil price, all of which have been affected by the possibility of sanctions and secondary sanctions. The other metals have largely been consolidating, albeit with an upward bias, while they wait for signs of a resumption of concerted global growth. With the sanction bubble somewhat deflated, at least for now, the outperforming metals are correcting and it seems the complex as a whole remains in a sideways trading pattern. There are now likely to be more cross currents for the markets to come to terms with. Reduced trade tensions could boost confidence in global growth again, but countering that higher bond yields could raise concerns of strong headwinds for global growth as debt servicing becomes more expensive.

Gold and the other precious metals prices are correcting and we put that down to the stronger dollar, with palladium reacting to developments over the Russian sanctions. For now we expect the stronger dollar to remain a headwind, but we expect support levels to hold.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW 24/04: Metals jumpy with prices reacting to strong dollar, latest sanction developments appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News