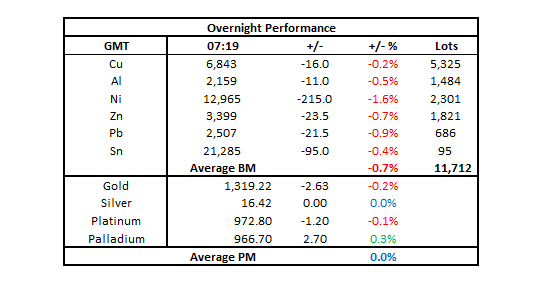

Precious metals prices remain subdued this morning, with gold (-0.2%) and platinum (-0.1%), and silver (flat) falling to capture haven bids in spite of the rise in risk aversion. Palladium (+0.3%) is the only precious metal showing a gain. We attribute the lack of upward pressure across the precious metals to the significant increase in US real rates, with the 10-year US Treasury Inflation-Protected Securities yield (proxy for US real rates) – at 0.76% – marking its highest level since December 2015. Although the rise in US real rates is driven primarily by a rise in nominal yields (rather than a fall in inflation expectations), this environment is not conducive to stronger precious metals pricing.

Precious metals could come under downward pressure in the immediate term should US real rates continue to grind higher. Given the Federal Reserve’s conviction that the recent bout of volatility is unlikely to last, investors revise more aggressively the present Federal Reserve tightening cycle. This is likely to exert upward pressure on the dollar and US rates, which in turn would be negative for the complex, especially gold.

Base metals traded on the London Metal Exchange are experiencing downward pressure this morning, Friday February 9, with the complex posting an average loss of 0.7% amid healthy volumes. Nickel (-1.6%) has been hit the worst, while copper (-0.2%) appears to be the most resilient.

The downward pressure across the industrial metals is driven by a deterioration in risk sentiment in Asia, evident in equity losses – the Shanghai Composite Index (~-4%) is down the most since February 2016 and the Nikkei 225 (~-2%) is at its lowest since October 2017. The worsening risk aversion in Asia is the result of negative spillover effects from the renewed surge in market fears in Thursday’s trading session in the Western world where the Cboe Volatility Index moved back up above 30, signaling that market participants remain on the cautious side, that is, reluctant to buy the dips with conviction.

This “risk-off” sentiment has induced broad-based deleveraging across the industrial metals, even though the recent data suggests that:

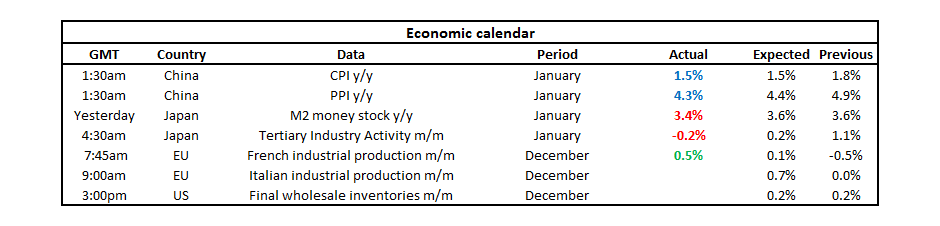

• Inflation dynamics in China are healthy (consumer inflation data released earlier this morning was in line with consensus)

• China’s demand for metal was robust in January (e.g. China’s refined copper imports in January were up by 17% year on year)

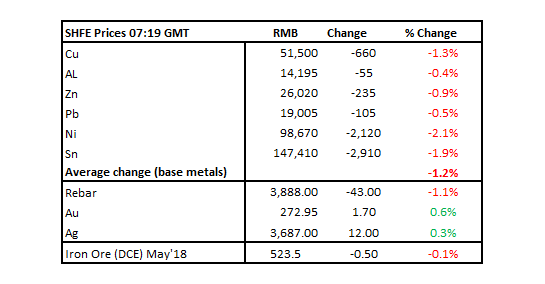

On the Shanghai Futures Exchange, the base metals are also experiencing broad-based weakness, showing an average loss of 1.2%, with nickel (-2.1%) the weakest and aluminium (-0.4%) the most resilient. The resilience of aluminium looks surprising following the recent China’s trade data, showing that exports rose by a stronger than expected 14.5% year on year in January. Copper prices in Changjiang are down by 0.6% at 51,170-51,450 yuan ($8,098-8,143) per tonne and the LME/Shanghai copper arbitrage ratio stands at 7.53, down slightly from 7.54 yesterday.

On the macro front, US Federal Reserve speakers continued to downplay the sudden surge in risk aversion earlier this month, inclined to leave unchanged their policy rate outlook. The economic calendar is quite light today, with investors likely to focus on industrial production numbers in Europe.

Base metals are likely to enjoy renewed strength after the recent wave of selling pressure. The present risk-off environment is unlikely to persist for too long considering that macro data releases continue to show improving global growth momentum. On the micro front, most base metals prices enjoy stronger supply/demand dynamics, evident in the fall in visible inventories for all base metals (excluding copper) since the start of the year. The “buying on the dips” mentality should therefore prevail.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post Metals morning view: Precious metals prices remain subdued this morning appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News