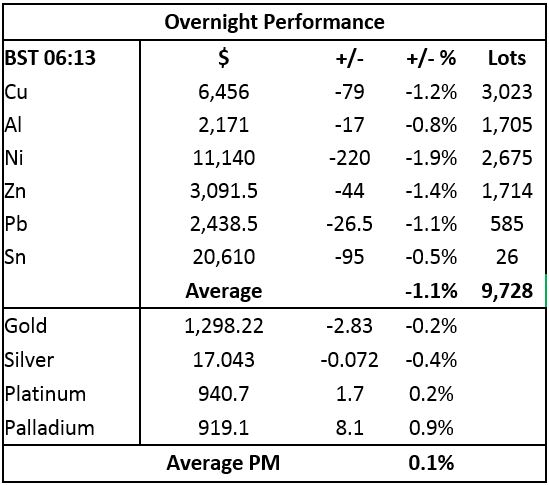

We were wary that the US Federal Open Market Committee (FOMC) statement could give the dollar a boost and that it could become a headwind for metals prices and that seems to have been the case. The base metals prices on the London Metal Exchange are down across the board by an average of 1.1% this morning, Thursday September 21.

Weakness ranges from a 0.5% fall in tin prices to a 1.9% fall in nickel prices, with copper prices down 1.2% at $6,456 per tonne – the low so far this morning being $6,441.50, which breached the lows from a week ago at $6,452.50.

The metals had started to look stronger on Wednesday, they closed up with average gains of 1.3%, so in some ways this morning’s performance seems a knee-jerk reaction. Although the rebounds seen earlier in the week could also have been bear-flags following the initial weakness that started around two-weeks ago. Volume has been above average with 9,728 lots traded as of 06:13 BST. High volume and price weakness does not bode well.

Precious metals prices are split, with bullion prices weaker while the platinum group metals are firmer. Gold and silver prices are down 0.2% and 0.4%, respectively, with gold prices at $1,298.22 per oz and silver prices at $17.04 per oz. In contrast, platinum prices are up by 0.2% at $940.70 per oz and palladium prices are up by 0.9% at $919.10 per oz. This follows a day of weakness on Wednesday when the complex closed down by an average of 0.8%, led by a 1.4% drop in platinum prices.

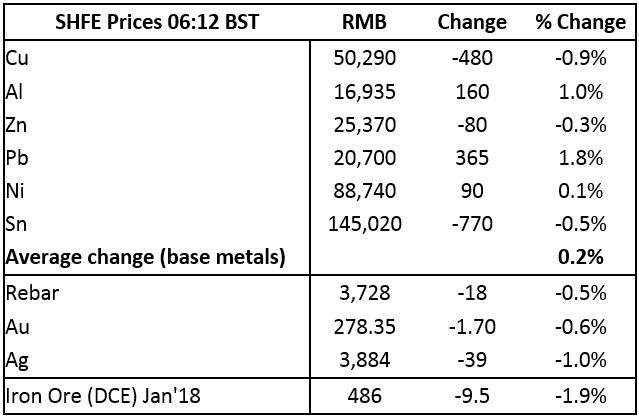

On the Shanghai Futures Exchange (SHFE) this morning, the base metals are mixed, with zinc, tin and copper prices weaker, the latter off by 0.9% at 50,290 yuan ($7,649) per tonne, while aluminium, lead and nickel prices are stronger. Lead prices are continuing to forge ahead with a 1.8% gain – see table below for more details. Given that the SHFE metals prices are not all lower, adds weight to our thoughts that the LME metals may be undergoing something of a knee-jerk reaction.

Spot copper prices in Changjiang are down by 0.8% at 50,260-50,460 yuan per tonne and the London/Shanghai copper arb ratio has climbed to 7.79, from 7.75 on Wednesday.

In this mixed picture for the metals, further weakness in steel rebar and iron ore prices are a negative factor. Steel rebar prices on the SHFE are down 0.5%, while January iron ore prices are down 1.9% at 486 yuan per tonne on the Dalian Commodity Exchange. Gold and silver prices on the SHFE are down 0.6% and 1%, respectively.

In international markets, spot Brent crude oil prices are little changed at $56.15 per barrel and given a more hawkish tone from the US Federal Reserve, the yield on US ten-year treasuries has climbed to 2.27%, while the German ten-year bund yield has eased to 0.44%.

Asian equities are mixed this morning with the Nikkei and CSI 300 up by 0.3% and 0.2%, respectively, while the Hang Seng and Kospi are down by 0.1% and the ASX 200 is off by 0.8%. This follows a mixed performance on Wednesday, where in the USA, the Dow closed up by 0.19% at 22,412.59, while in Europe, the Euro Stoxx 50 dipped 0.16% 3,525.55.

The more hawkish Fed stance, with FOMC saying it would start reducing its balance sheet from October has given the dollar a boost, with the dollar index rising to 92.55 – we wait to see if that is enough to turn the trend in the dollar, or whether the downward trend will continue to dominate. The direction of the dollar may now become a major factor in which direction the metals take in the weeks ahead. Against the stronger dollar, the euro at 1.1883 is weaker, as are sterling at 1.3487, the yen at 112.45 and the Australian dollar at 0.7974.

The Chinese yuan has been weakening since September 8 – it continues to do so and was recently quoted at 6.5891. Most of the other emerging currencies we follow are weaker in line with the stronger dollar.

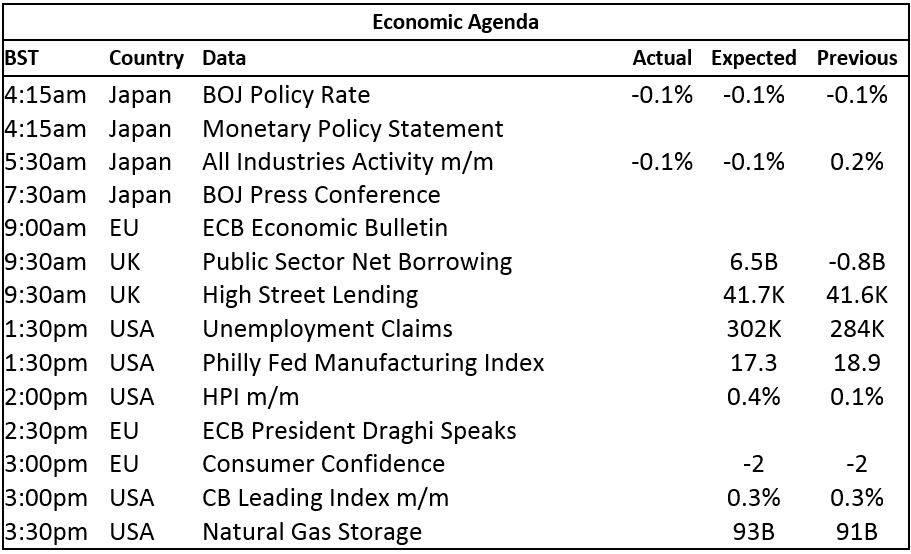

Data out already shows Japan left interest rates unchanged at 0.1% and it will continue with its asset buying programme, while its all industries activity dipped 0.1%, after a 0.2% climb. Later there is a European Central Bank (ECB) economic bulletin, UK data on public sector borrowing and high street lending, with US data including initial jobless claims, the Philly Fed manufacturing index, the house price index, CB leading indicators and natural gas storage. In addition, ECB president Mario Draghi is speaking at 14:30 BST.

As Europe opens, the base metals are looking heavy and copper is looking vulnerable to starting another leg down in its correction. The rest are looking vulnerable but not to the same extent as the copper chart does. As such, we wait to see if there is follow-though selling as the European day unfolds, or whether the dip buyers come in. Today’s and tomorrow’s action on the base metals and the dollar, are therefore likely to set the tone for a while.

The strong tone from the Fed and the fact they seem to be more definite about where they are heading, is weighing on gold prices. We have seen the pullback in gold price as the market testing its break out level from the continuation pattern – the top of which was $1,295 per oz. So far the low since the FOMC statement has been $1,295.95 per oz. A break below support would open the way for further weakness, especially if it coincides with a further rebound in the dollar. The other precious metals are following gold’s direction, especially silver and platinum, while palladium seems to be running into some support ahead of the $900 per oz level. With gold testing support, trading is likely to remain nervous for a while.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW: Gold prices testing $1,295 per oz support following FOMC statement appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News