Base metals prices on the London Metal Exchange are heading lower again by an average of 0.6% this morning, Tuesday September 12. Three-month nickel prices lead the way with a 1.6% drop to $11,645 per tonne, copper and tin prices are off by 0.6%, with copper at $6,709 per tonne, while the rest are off by between 0.2 and 0.3%. Volume has been average at 5,750 lots.

This follows a day of rebounding prices on Monday, when the complex rebounded 1.4% after an average fall of 3% on September 8. We expected the pullback to last longer than just a day so are not surprised prices are weaker again – we should now get a feel for how bullish underlying sentiment is by seeing how well supported the dips are.

Precious metals are split with palladium prices up by 0.4% at $937.30 per oz, while gold and silver prices are down 0.4%, with spot gold at $1,323.98 per oz, and platinum prices are off 0.1%. This follows a general day of weakness on Monday, where the complex closed off an average of 0.9%.

On the Shanghai Futures Exchange (SHFE) this morning, the base metals are firmer across the board by an average of 1% – seemingly as they follow the LME’s rebound from Monday. The main gainers today have been aluminium prices (+2.9%), zinc prices (+2.3%) and lead prices (1%), while nickel and tin are up 0.1% and 0.2%, respectively, and copper prices are up 0.4% at 51,550 yuan ($7,873) per tonne. Spot copper prices in Changjiang are up 0.6% at 51,330-51,560 yuan per tonne and the London/Shanghai copper arb ratio has edged higher to 7.68, compared with 7.66 on Monday.

Steel rebar prices on the SHFE have halted their decline for now with a 0.2% price gain, similarly iron ore prices for January delivery have rebounded, with prices up 1.1% at 536 yuan per tonne on the Dalian Commodity Exchange. Back on SHFE, gold and silver prices are down either side of 0.6%.

In international markets, spot Brent crude oil prices are down 0.38% at $53.70 per barrel and the yield on US ten-year treasuries has jumped to 2.13% as the UN sanctions were not as harsh as the USA wanted, while the German ten-year bund yield has edged higher to 0.34%.

With the North Korean situation somewhat calmer, at least for now, equities in Asia are stronger as focus turns to the economic outlook rather than geopolitical issues. Gains are as follows: the Nikkei (+1.15%), the CSI 300 (+0.61%), ASX 200 (+0.6%), the Kospi (0.13%) and the Hang Seng (+0.09%). US markets were stronger too as Hurricane Irma has passed and North Korea avoided raising the ante by not firing any missiles over the weekend or on the anniversary of 9/11 – the Dow closed up 1.19% at 22,057.37, while in Europe the Euro Stoxx 50 climbed 1.38% to 3,495.19.

The dollar index is attempting a rebound, at 91.87 it is recovering from fresh multi-year low at 91.01 on September 8, the euro at 1.1963 is edging lower, sterling is firm at 1.3184, the yen is weaker at 109.36 as is the Australian dollar at 0.8024. So we are still waiting to see if spikes in the dollar and currencies on September 8 were a turning point.

The Chinese yuan is weaker again today, it was recently quoted at 6.5300, from a peak of 6.4345 on September 8. The relaxation in restrictions on shorting the yuan has led to this weakness. The slightly stronger dollar seems to be halting the firmer tone in the other emerging market currencies we follow.

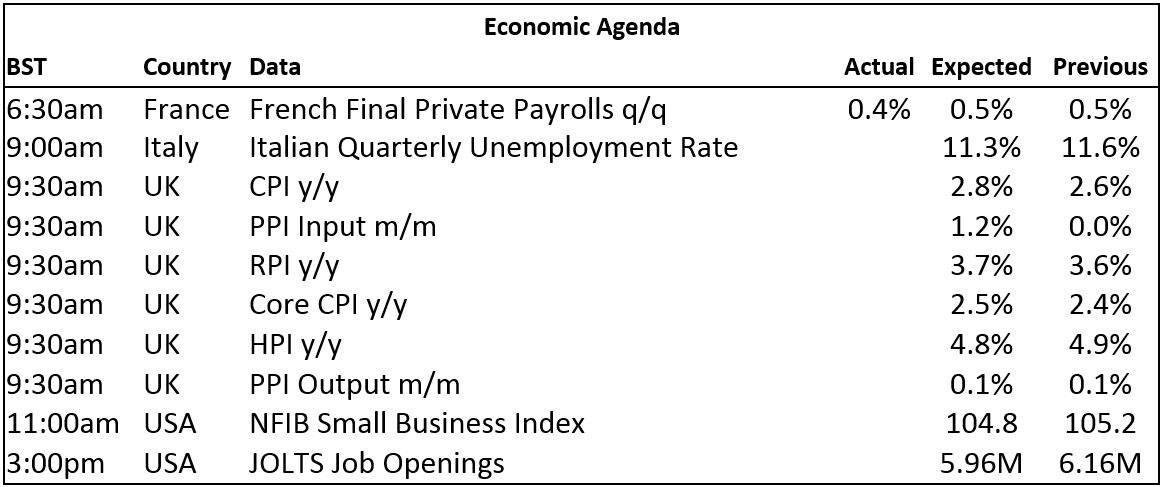

Data out already today showed France’s private payrolls climb 0.4%, below the 0.5% expected and seen previously. Later there is data on Italian unemployment, a host of UK price data, with US data including a small business index and job openings.

The corrections in the LME metals prices on September 8 were to some extent expected and overdue as it has recently felt like prices had run ahead of the fundamentals. Dip buying was seen on Monday, but it appears selling pressure is around again this morning. We wait to see if underlying bullish sentiment is strong enough to step in already, or whether there is enough doubt around to see more profit-taking and pricing. Given the gains seen since May, we would not be surprised to see a bit more price weakness – a 38.2% Fibonacci retracement for example would take copper prices back to around $6,400 per tonne. That said, we remain overall bullish for the metals, but question whether enough potential buyers will be willing to chase prices higher from these already rich price levels. As such, we would let this correction run its course before looking to enter the market again.

Gold prices are correcting recent strength, the latest UN sanctions against North Korea did not include a limit on oil imports that the USA wanted so tensions may calm down for a while, especially as there are some reports that North Korea officials are planning informal talks with former US officials. On the charts, the precious metals prices are looking a bit toppy and with the dollar attempting to rebound, gold prices may face more profit-taking.

Metal Bulletin publishes live futures reports throughout the day, covering major metals exchanges news and prices.

The post METALS MORNING VIEW: Gold prices retreat as dollar rebounds appeared first on The Bullion Desk.

Read More

Source: Bullion Desk News